The Weekly Anthropocene, June 21 2023

Mycorrhizal fungi in the carbon cycle, electric cars zooming ahead, "neighborhood geothermal," a renewables milestone for Europe, and more!

European Union

In May 2023 in the European Union, wind and solar produced more electricity than fossil fuels, for the first time ever. Wind and solar combined produced 30.65% of the EU’s electricity, compared to 27.26% for oil, coal, and natural gas combined. (See chart). Relatedly, coal power hit an all-time monthly low in the EU, providing just 10% of electricity. And the remaining 42.08% of electricity was produced by other non-fossil power sources, like France’s fleet of nuclear power plants and Scandinavia’s multitude of hydropower dams, so this is getting close to a fully renewable grid! True, May in Europe tends to be a relatively windy and sunny time of year, so the total percentages for 2023 probably won’t be quite as good, but the upward trend for clean energy is clear and inexorable. This is an epic, historic first. And even better, it will soon become normal, even unremarkable, in the EU and many other jurisdictions. Renewables: they get the job done!

Electric Vehicles

Bloomberg released their Electric Vehicle Outlook 2023 report. Some key highlights:

By 2026, EVs are on track to reach 52% of new passenger vehicle sales in China, 42% in Europe, 30% globally, and 28% in the US.

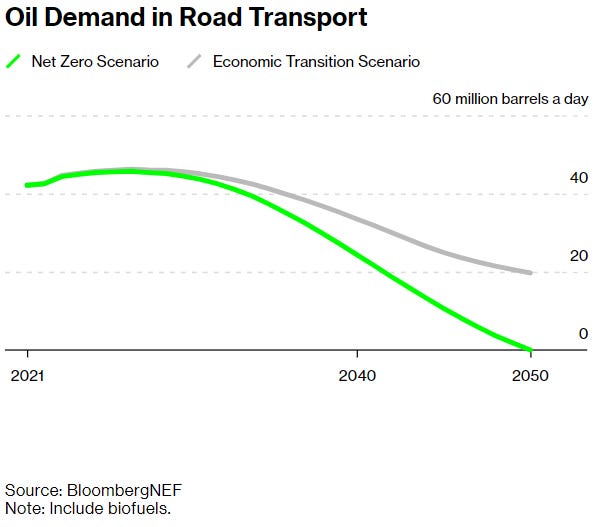

Oil demand for road transport is likely to peak by 2027 globally and by 2024 in China. It’s already peaked in America and Europe. (See chart). Even in Bloomberg’s less optimistic “baseline” Economic Transition Scenario, global oil demand will decline by more than 50% by 2050.

Sales of combustion-engine cars “peaked six years ago and are now in long-term decline.”

Global spending on EV battery factories is “ahead of schedule,” on track for what would be required for the optimistic “net-zero emissions by 2050” scenario.

Global demand for lithium, a vital EV battery mineral, may rise as much as 22-fold by 2050, though this could be substantially reduced if new lithium-less technologies like sodium-ion batteries do well.

United States

As this newsletter has widely chronicled, the Inflation Reduction Act has fueled an economy-reshaping boom in American clean energy manufacturing (see chart), with an associated jobs surge. Notably, this could be a major plus for Democrats in the 2024 presidential elections, especially given that the five key swing states of Georgia, Michigan, Nevada, North Carolina, and Arizona have each received over $1 billion in new EV supply chain investments. Note that the chart above is all US manufacturing, not just EV or battery-related: the renewables revolution is now a key motor of economic growth in America.

Canadian Solar announced that they’re building a $250 million, 1,500-job solar panel factory in Mesquite, Texas. Once it’s complete (by the end of 2023), it should produce 5 GW (5,000 MW) of solar panels per year. Another wave in the rising tide of US clean manufacturing wins!

The U.S. EPA is starting a new Inflation Reduction Act-funded “Solar for All” grants program, making a fund of $7 billion available for up to 60 projects working to expand residential and community solar in low-income and disadvantaged communities. States, municipalities, tribes, and nonprofits are all encouraged to apply: the EPA plans to eventually make at least one award per US state and territory.

A new report from Dartmouth, Princeton, and the BlueGreen Alliance has calculated that thanks to the Inflation Reduction Act (specifically the 45X MPTC tax credit for clean manufacturing), it will shortly be cheaper for American energy projects to use American-made solar and wind components than imported solar and wind components. Once the huge wave of new solar panel factories currently in the pipeline are built, they estimate that 100% US-made solar panels will be 30% cheaper than imported solar panels. The report also forecasts that an additional 4 million solar and wind jobs will be created in coming years. The Biden Administration’s pioneering decarbonization industrial policy is looking good!

The Department of Energy has created a new Energy Savings Hub, at energy.gov/save, to guide Americans through accessing the Inflation Reduction Act’s bonanza of clean energy tax credits. If you’re a US taxpayer, check it out!

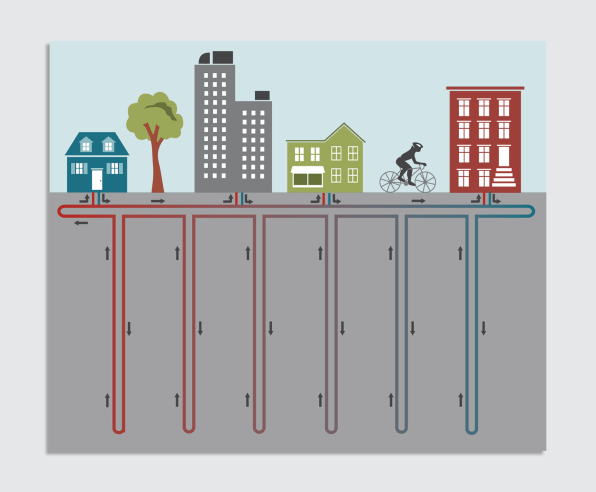

A “neighborhood geothermal” project in Framingham, Massachusetts is drawing global attention as a decarbonized heating solution. The local gas utility, Eversource, has partnered with the Home Energy Efficiency Team (HEET) nonprofit to build a network of looped geothermal pipes connecting 40 buildings (including homes, apartments, businesses, and a fire station). In the winter, the liquid will be pumped underground to heat up (like standard single-home geothermal heating systems), then back up into heat pumps to warm the buildings. (See HEET diagram above). In the summer, the process will be reversed, with heat from the buildings sent underground to provide air conditioning. This innovative, cost-saving model is likely to rapidly spread across the country: 13 other utilities nationwide are discussing similar partnerships with HEET, and 17 neighborhood geothermal pilot projects are already being planned in New York State alone!

In 2022, the Mountain Pass mine in California produced 42,499 metric tonnes of rare earth elements1, 14% of the global total that year. Now, in mid-2023, the Mountain Pass mine plans to start separating out rare earths from dross metals-the first time this processing step has happened in the US since 2015. The interesting thing about this is that Mountain Pass is the only large-scale rare earth element mine in the Western Hemisphere, and it was moribund as recently as 2017, when it was bought and refurbished by a new company following the previous owners’ bankruptcy. So this is an impressive turnaround! And it's being done sustainably as well, operating as a “zero discharge” facility with all water recycled on-site and all non-liquid waste buried in lined landfills.

This is encouraging news! The fact that reopening one single mine got the US from near-zero to 14% of global total rare earth production indicates that it is in fact quite easy to ramp up rare earth production2, and that this won’t likely be a serious supply bottleneck for the renewables revolution.

Mycorrhizal Fungi

A paradigm-shifting new study found that mycorrhizal fungi, the underground fungal networks living symbiotically with plants around the world, are a previously unknown global carbon storage pool. An analysis of an array of different plant-fungi studies from around the world calculated that plants on Earth likely pass over 13 billion metric tonnes of CO2-equivalent to their fungal symbiotes every year (generally in the form of the carbohydrates that plants channel to fungi in exchange for water and minerals), or about 36% of humanity’s annual CO2 emissions from fossil fuels. To clarify, this doesn’t mean that Earth’s biosphere as a whole is sequestering more carbon than we thought-this carbon was already “counted” as being taken up by plants during photosynthesis, but we’re now learning that a lot of plants’ carbon ends up in mycorrhizal fungi. As The Weekly Anthropocene discussed in a review of Entangled Life, we’re only beginning to understand the complex roles that fungi play in the chaotic orchestra of life on Earth, and it now looks like they are a key nexus in the biogeochemical carbon cycle as well. Fascinating news!

A recap: “rare earths” refers to a group of 17 very similar elements, from dysprosium to neodymium to praseodymium, that aren’t actually particularly rare in Earth’s crust but are very difficult to extract because they’re mixed in with other metals. They all have strong magnetic fields, making them critical ingredients for the industrial magnets used in wind turbines, EV motors, drones, tanks, aircraft, advanced lasers, and a bunch of other valuable stuff. Lithium is not a rare earth: it’s much more common, much less magnetic, and much easier to mine, but it’s also critical for a lot of battery technologies. Copper and cobalt aren’t rare earths either, but they’re also “critical minerals” as designated by the US Geological Survey. Almost all rare earths are critical minerals, but not all critical minerals are rare earths. These are the metals we need more of for the clean energy transition to work. (And mining for all of this still adds up to hundreds to thousands of times less mining than is currently needed to keep the economy running on fossil fuels: check out Dr. Hannah Ritchie’s definitive article on the subject).

As readers of The Weekly Anthropocene may recall from our interview with economist Noah Smith earlier this year.